Over the last few weeks, I’ve been getting a lot of queries with respect to the current volatility in Indian Equity markets and one question: what do the last 40 years of Indian equities really teach us about long-term investing?

One common theme when extreme events happen is that news headlines keep predicting the end of the world and a lot of negativity in general, but the market keep quietly doing what it does best: endure, recover and compound.

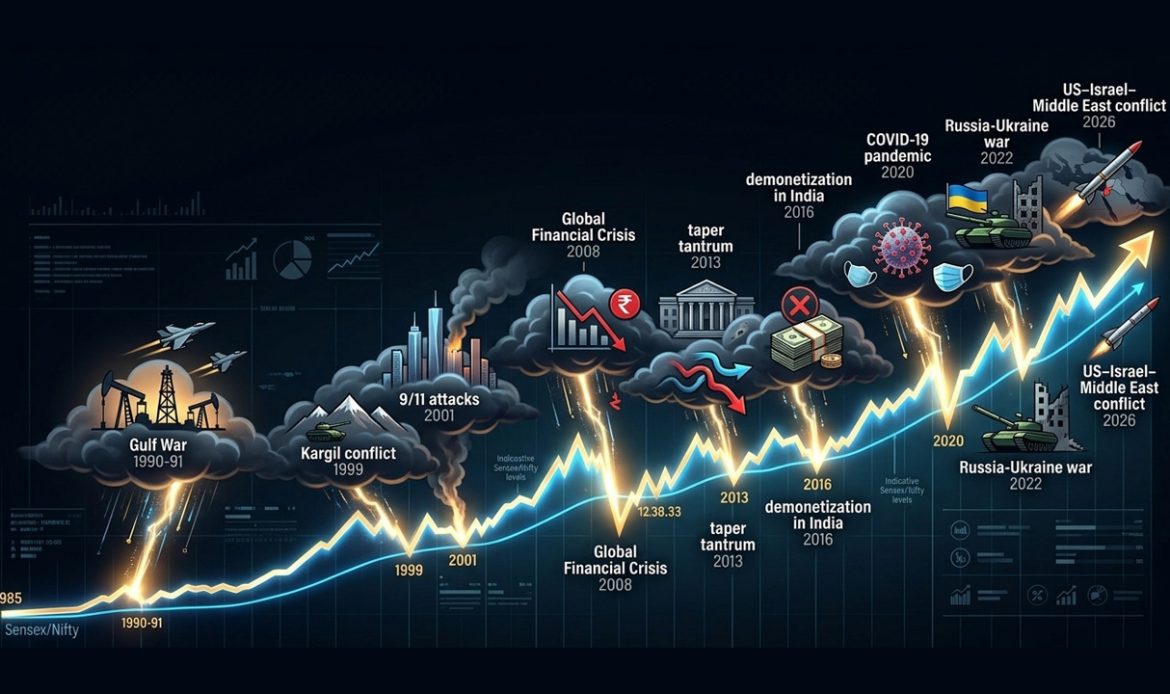

Living through “the end of the world”

If one has invested in India for any reasonable length of time, they’ll recognise the feeling: every few years, there is a new crisis that feels like this is the one that will finally break the system.

In my own journey and in conversations with investors, I’ve seen the same pattern repeat around wars, scams, pandemics, currency shocks and political upheavals. Each episode comes with dramatic headlines, bold TV graphics, and confident forecasts of collapse. And yet, when I zoom out, even the scariest crashes shrink into brief dents on an otherwise rising curve.

Since the mid1980s, the Sensex and Nifty have navigated over 20 major crises: from the Gulf War and Kargil to 9/11, the Global Financial Crisis, the taper tantrum, demonetization, COVID, and the Russia-Ukraine conflict. Each time, patient investors who stayed were ultimately rewarded.

What the last 40 years really say

If we strip away the noise and just look at the numbers, the story became simple.

Over the last 40 years, Indian equities have compounded in the 14%+ CAGR range, turning disciplined SIPs and lumpsum investments into serious wealth.

This is the uncomfortable truth markets keep trying to teach us:

- Market falls are frequent and often violent, but not permanent

- Recoveries are not guaranteed in a straight line, but they have been remarkably consistent over decades in India’s growth story

- Compounding rewards patiencefar more than cleverness.

- The only strategy that has worked across cycles is to stay the course.

My biggest takeaway: Why does it work every time?

Where is the economy headed? And how is the earnings growth of Nifty50 – the broader benchmarks vis-a-vis the current Equity market valuations?

With a balanced fiscal discipline resulting in 7% Real GDP growth rate possible with 7% inflation going forward with a Nominal GDP growth of 14%. Nominal GDP has been around 11%-13% over the last 40 plus year period which is reflecting in the 14%-15% EPS growth of Nifty50 resulting in 14% Equity market returns over the long term.

Historically Nifty50 Price Earning multiple has been 18-22& currently it stands at 20.30x for FY 2026 and 17.90 as per FY 2027 earnings. Historically this PE multiple is considered cheap and with earnings growth expected to be at 14%-15%.

How I choose to invest

My personal philosophy has always been clear and simple. I am pragmatic and do not want to build my financial life around predictions, narratives or short term forecasts. Instead, I want to build it around participation: in India’s growth story, in the compounding power of good businesses, and in a process that I can stick with through cycles.

For me, that means:

- Accepting volatility as rent I pay for longterm equity returns

- Volatility is a feature and not a bug to generate long term returns

- Using sharp declines not as exit signals but as opportunities to invest more

- Measuring success not over months or even a couple of years, but over five plusyears and the best way to measure is over decades.

When I look back at 40 years of Indian equities, I don’t see a straight line; I see a series of storms, each of which felt like the end of the world in real time. Yet the market endured, recovered, and compounded ultimately resulting in Wealth Creation.

That, ultimately, is the lesson I’m choosing to live by.